How to Get Out of Merchant Cash Advance Debt in 2026: A South Florida Owner's Refinance Playbook

You took the advance because the money hit your account in 48 hours and payroll was due Friday. Now there are two, maybe three, maybe four withdrawals clearing your account every single business day, and you're refreshing your bank balance at 6 a.m. to see who got paid first. You're winning contracts, your crews are busy, and you still can't breathe. If that's you, read this before you take one more dollar. You are not stuck — but the way out is specific, and the wrong move makes it worse.

We talk to South Florida service business owners every week who are servicing merchant cash advances at effective rates they never actually saw on paper. Good businesses — profitable, growing, well-run — get caught in this because the product is built to feel like a lifeline and priced like a payday loan. This is why it's so hard to climb out on your own, and the exact sequence that gets solid businesses back to affordable capital.

What's Actually Happening

Merchant cash advances are not loans. Legally, they're a sale of your future receivables, which is how they sidestep state usury caps. That structure is why the cost is quoted as a "factor rate" — 1.4, 1.5 — instead of an APR. A $100,000 advance at a 1.45 factor means you repay $145,000, and if the funder pulls it back over six months through daily ACH debits, the effective annualized cost lands somewhere between 40% and 150%. In the worst stacked cases it runs higher. In January 2025, the New York Attorney General secured a $1.065 billion judgment against Yellowstone Capital and 25 affiliated entities, with the court finding their advances were actually loans carrying rates as high as 820% and ordering debt cancellation for more than 18,000 businesses. That's the extreme end, but it tells you what this market can do when nobody's checking the math.

Here's why it's spreading. More than 76% of small businesses now bypass traditional banks for capital — an all-time high — and the fast-money lenders filled that gap with slick applications and same-day approvals. Cash flow, for the first time, is the number one concern owners report, ahead of inflation. The online and fintech lenders now hold an estimated $70 billion-plus in outstanding small business balances. So the demand is real, the product is everywhere, and the marketing is relentless — you probably get three MCA offers in your inbox a week, each one dangled right when your account is tight.

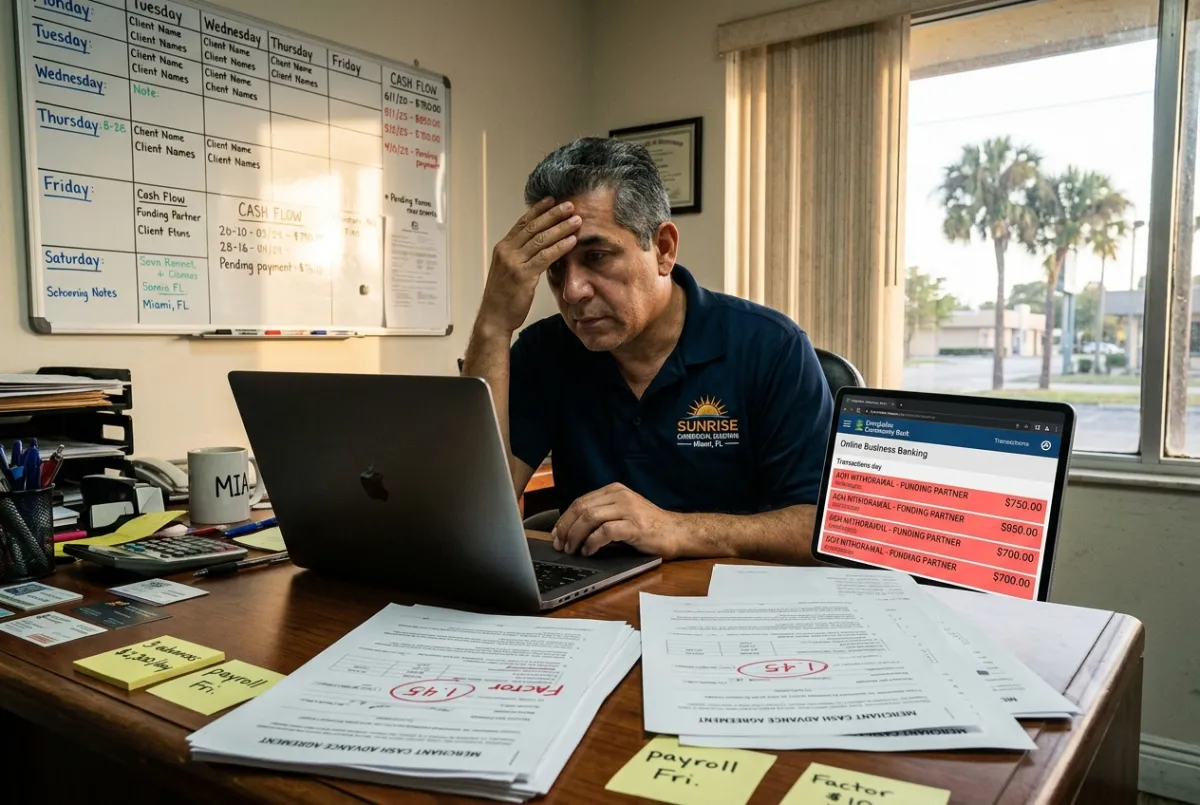

A Bayside client — a Broward County commercial cleaning company doing about $2.1M a year — came to us with three advances stacked on top of each other. Combined daily debits were pulling roughly $2,300 out of the account every business day. The business was profitable on paper and drowning in practice. He'd taken the second and third advances to make payments on the first, and each new funder charged a little more than the last because his file looked riskier every time. By the time he called me, he was choosing which vendor to pay late each week and had started factoring personal savings into payroll. That's the tell: when new money exists only to service old money, you don't have a cash flow problem anymore, you have a structure problem. Nothing about his business was broken. His revenue was fine. What was broken was the shape of his debt — short, daily, and stacked — sitting on top of a business whose cash comes in on 30- and 45-day net terms. The timing mismatch alone was strangling him.

Why It Matters and What Owners Get Wrong

The mistake almost everyone makes is treating the symptom. The account is tight, so they take another advance to loosen it. It works for about two weeks. Then the new daily debit joins the others and the hole is deeper than before. Stacking is the single fastest way to destroy a business's borrowing future. Every advance files a UCC lien against your receivables, and those filings are public. By the third one, your business looks radioactive to any real lender — a bank underwriter sees four funders with first claim on your cash and closes the file without a second call. You didn't just get expensive money; you signaled to the entire lending market that you're in distress.

It gets more expensive than the interest, too. Daily debits wreck the one thing SBA and bank underwriters care about most: consistent, positive cash flow in your business bank statements. Underwriters spread your last three to six months of statements and count the negative days, the NSF fees, the pattern of small withdrawals. When your statements show a dozen daily debits and frequent overdrafts, you can't qualify for the cheap capital that would actually solve the problem — a 10.5% SBA loan or a 9% term loan — precisely because you're buried in 100%-plus money. It's the cruelest part of the trap: the MCA makes you look exactly like the borrower who can't get out of the MCA. The advance doesn't just cost you today; it locks you out of the exit for six months to a year even after you've stabilized.

And it follows you when you sell. Any buyer doing real diligence pulls your UCC filings and your bank statements. Stacked advances signal distress and depress your multiple, or blow up the deal entirely — I've had buyers walk from otherwise clean deals the moment they saw four active liens. Even if the debt is paid off, unreleased UCC filings sit on record and slow your closing while lawyers chase terminations. I've watched owners lose six figures of enterprise value at exit because of a cash-flow patch they took three years earlier and never cleaned up. The downstream damage — SBA ineligibility, killed bank relationships, a lower sale price, a spooked buyer — almost always dwarfs the original shortfall that sent them to the MCA in the first place. The advance solves a $40,000 problem and quietly creates a $200,000 one.

The other thing owners get wrong is waiting too long to ask for help. The best time to refinance an MCA is before you take the second one. The second-best time is now, while the business is still generating cash and you still have leverage. Once you're missing debits and funders are calling, your options narrow fast and get more expensive.

What to Do Instead

If you're in it, work the problem in this order:

Stop stacking. Today. No new advance solves an advance problem — it just moves the crisis two weeks down the road and makes it bigger. Draw the line before you do anything else, even if it means a hard conversation with a vendor this week.

Map the real cost. List every advance: funder, balance owed, daily or weekly debit, and remaining term. Convert each factor rate to an effective APR so you can see what you're actually paying. Most owners are genuinely shocked when they see the blended number on one page. You can't fix what you won't measure.

Pursue true consolidation or refinance — not another advance dressed up as one. A genuine consolidation replaces your MCAs with a single longer-term loan or line of credit at 12–36 month terms, dramatically below MCA cost, with one predictable monthly payment instead of a dozen daily hits. Watch out: most "consolidation" offers from MCA brokers are just a fourth advance layered on top. If it still debits daily and quotes a factor rate, it's not a consolidation.

Check SBA and community-bank options first. If your business is fundamentally profitable, an SBA 7(a) refinance or a community-bank term loan is the cheapest exit, and refinancing high-cost debt is a legitimate, common use of SBA proceeds. It's harder to qualify while you're still debited daily, which is exactly why sequencing and timing matter — start the conversation before your statements deteriorate further.

Get a second set of eyes before you sign anything. The paper is written to be confusing on purpose. Have someone who works for you — not the funder, not the broker collecting a commission on the next advance — read the terms and tell you the real cost and the real risk.

Frequently Asked Questions

Can you actually refinance or consolidate MCA debt? Yes, but be precise about the word. Real consolidation swaps your advances for one lower-cost loan or line of credit with a longer term and a single predictable payment. The catch is that a lot of what's marketed as "MCA consolidation" is just another advance with a nicer brochure. If the payoff still debits your account daily and the cost is quoted as a factor rate instead of an APR, it's not a fix — it's the fourth stack. The real thing exists, but you have to know what you're looking at.

Will getting out of an MCA hurt my credit? Paying off an advance on schedule doesn't hurt you — it helps, because it clears the UCC liens and cleans up your bank statements, which is exactly what the next lender wants to see. What hurts is defaulting, which can trigger a confession of judgment and personal-guarantee enforcement, and in bad cases a funder freezing your receivables. The goal is an orderly payoff, not a missed one. If you're heading toward a missed debit, that's the moment to get help, not after.

Is an MCA the same as a loan? No, and that distinction is the whole game. An MCA is legally a purchase of your future receivables, which is how funders avoid state usury limits and quote cost as a factor rate instead of an APR. Because it's not structured as a loan, a lot of consumer and small business lending protections don't apply the same way. That's also why the true cost is so easy to miss — nobody is required to show you an APR, so you don't see the 90% until you do the math yourself.

How much does a merchant cash advance really cost? Depending on the factor rate and how fast it's repaid, effective annualized cost typically runs 40% to 150%, and higher on stacked or aggressive deals — remember, the faster they pull it back, the higher the effective rate. Compare that to roughly 9.5–11.5% on an SBA loan or 15–30% on a solid term loan, and the math makes the decision for you. The factor rate hides this; a $50,000 advance at 1.49 repaid in five months isn't "49% money," it's closer to triple that annualized.

Can I still get an SBA loan if I have MCAs? Sometimes — and refinancing MCA debt into an SBA loan is a legitimate, recognized use of proceeds. But the daily debits and negative bank-statement days make qualifying harder while the advances are active, because underwriters see the same distress signals a buyer would. The sooner you start the conversation, the more options you keep. Waiting until you've missed payments is the worst version of this problem.

How fast can I get out of MCA debt? It depends on your numbers, but a realistic consolidation or SBA refinance timeline runs anywhere from a few weeks to a couple of months from a clean application. The variable is usually documentation and how many funders have to be paid off and release their liens. The businesses that move fastest are the ones that mapped their advances early and started before they were in crisis — another reason not to wait.

Should I just stop paying and try to settle? Be very careful here. Settlement and "debt relief" firms exist, and in genuinely distressed situations restructuring can be the right path — but stopping payments unilaterally can trigger confessions of judgment, frozen accounts, and lawsuits that are far worse than the debt. Don't take that route on advice from anyone who profits from selling you the next product. Get a neutral read on whether refinance, consolidation, or restructuring actually fits your situation before you stop a single debit.

Let's Look at Your Situation

If you're servicing one advance or four, the worst thing you can do is nothing — and the second worst is taking another one. Send us your situation and we'll walk through your real numbers, tell you honestly whether a consolidation, refinance, or SBA path fits, and give you a straight answer with no obligation. Start here: https://baysidebusinessadvisors.com/submit