Line of Credit vs. Term Loan: What South Florida Service Business Owners Get Wrong — And What It Actually Costs Them

You needed capital. Maybe payroll was tight, maybe you had a build-out to fund, maybe an opportunity showed up faster than your cash flow could handle. So you called around, got approved, and took what moved quickest. It felt like a win.

Six months later, something is off. The line of credit you opened is maxed and not revolving the way you expected. The term loan has a fixed payment that doesn't care about your slow season. You're not in crisis — but you're tighter than you should be, and the next time you need capital, you're going to have a harder conversation with a lender than you had the first time. The product wasn't wrong. The match was.

For service business owners doing $500k to $5M, this mismatch is one of the most common and most expensive mistakes I see — and it rarely shows up on your P&L until it's already cost you something meaningful.

What's Actually Happening in the Market

Lines of credit and term loans are both legitimate, widely used tools. But they are built for completely different jobs, and in 2026, the funding environment is making it easier than ever to grab the wrong one.

Banks have tightened underwriting standards on small business loans — particularly commercial and industrial lending — which means more owners are turning to online and alternative lenders. Those lenders move fast, approve at higher rates, and are often indifferent to whether the product they're selling fits your actual need. You apply, you get approved, you take the money. Nobody asks what you're using it for.

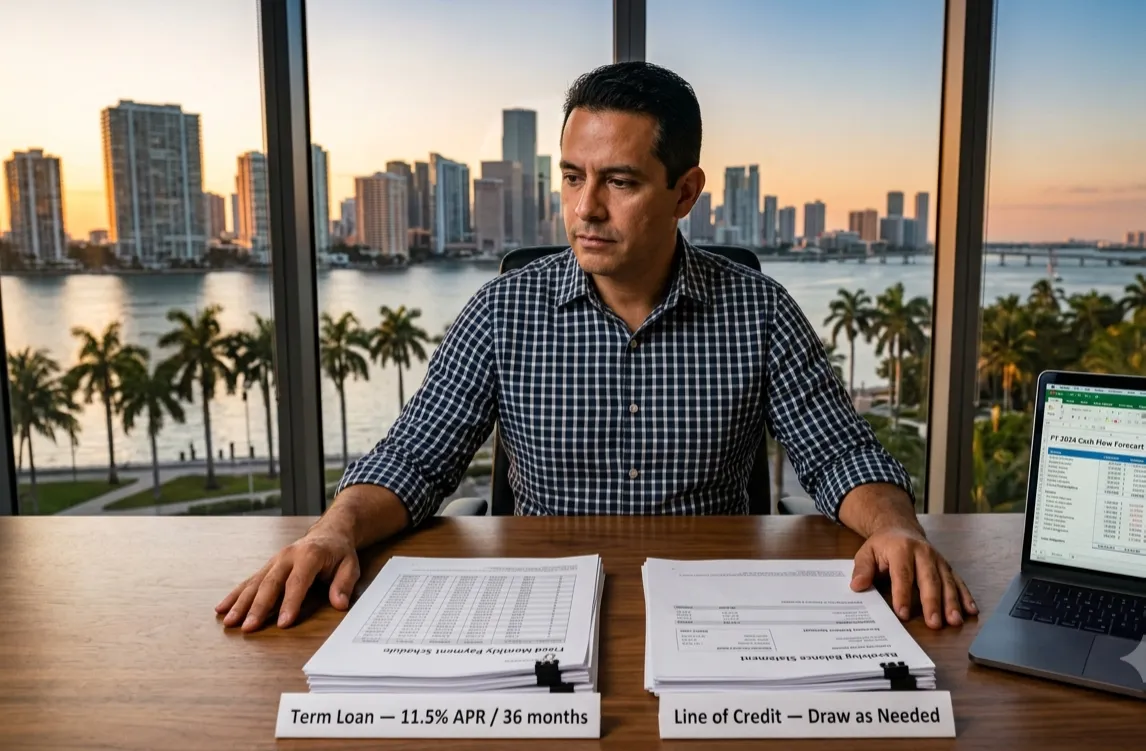

Here's the core distinction that matters. A business line of credit is revolving — you draw what you need, repay it, and draw again. You pay interest only on what you've borrowed. It's designed for variable, recurring, short-term needs: bridging a gap between when you invoice and when you get paid, covering payroll during a slow stretch, restocking inventory before a busy season. It's a cash flow tool.

A term loan is the opposite. You receive a fixed lump sum upfront and repay it on a set schedule — usually at a fixed rate — over a defined period. It's built for planned, one-time investments with a known cost and a clear return horizon: a build-out, a piece of equipment, an acquisition, debt consolidation. It's a capital investment tool.

I had a client last year — a $2.2M landscaping operation out of Broward County — who came to me with what looked like a cash flow problem. When we pulled his debt schedule, the real issue was structural. He'd taken a term loan eighteen months earlier to fund two new trucks. Smart use of a term loan. But when a slow quarter hit, he'd drawn his line of credit all the way down to cover operating expenses — and the line never fully revolved because he was also making fixed loan payments on the trucks. Both products were doing their job. They just weren't designed to carry that load simultaneously, and together they were choking his monthly cash position. We restructured the debt. It took three months and cost him in fees and opportunity. The mismatch cost more than the interest ever did.

Why It Matters — And What Owners Get Wrong

The most common mistake I see is using a line of credit to fund something long-term, or using a term loan to solve a short-term cash flow problem. Both feel reasonable in the moment. Both create problems that compound over time.

When you use a revolving line of credit to fund a renovation, buy equipment, or make a capital investment, a few things go wrong at once. First, the cost climbs. Line of credit rates in 2026 are running 8% to 16% APR for most service businesses — variable, and exposed to rate movement. If you're carrying that balance for a year or two instead of cycling it the way a revolving line is designed to work, you're paying more than you would have on a fixed-rate term loan. Second, you've tied up your revolving capacity. A line of credit that's sitting at 80% or 90% utilization isn't a safety net — it's a liability. When a real cash flow gap hits, the tool you built for exactly that situation isn't available.

The reverse mistake creates a different problem. Using a term loan to smooth out operating cash flow puts you on a fixed repayment schedule that doesn't flex with your revenue. A slow month, a late-paying client, a dip in the back half of the year — those fixed payments keep coming regardless. And if you've committed to a 36- or 48-month payback on working capital that's long since been spent, you're carrying dead debt against future revenue.

What most owners don't see until it's too late is the downstream effect on their financing options. SBA underwriters, bank credit officers, and — if you ever sell the business — buyers and their lenders all look at how you borrow, not just how much. A line of credit perpetually above 80% utilization is a red flag regardless of what your revenue looks like. A term loan taken for an operational gap rather than a capital investment can distort your debt service coverage ratio, which is one of the primary metrics SBA lenders use to determine 7(a) eligibility. If you're planning to pursue an SBA loan in the next 12 to 24 months — for growth, an acquisition, or a refinance — your current debt structure is either building that case or quietly undermining it. The same is true if you ever want to sell. A sophisticated buyer's lender will look at your capital stack in due diligence, and mismatched debt tells a story you don't want told.

What to Do Instead

Getting the match right isn't complicated once you understand the logic. Five rules that work:

1. Match the structure to the life of the need. If the expense is short-term, recurring, or variable — payroll gaps, inventory, bridging receivables — that's a line of credit. If the expense is a one-time investment with a defined cost and a clear payback window, that's a term loan. The question isn't which product feels easier to get. It's which product was designed for what you're actually doing.

2. Match the repayment timeline to the asset's useful life. If you're financing equipment that will generate revenue for five years, a five-year term loan makes sense. Funding that same equipment with 12-month revolving draws does not — you'll drain your revolving capacity before the asset pays you back. Align the debt to the asset, not to what was available.

3. Keep your line of credit below 50% utilization. A line below 50% is a tool. A line above 80% is a warning signal to every lender who pulls your file. If your line is perpetually maxed, that's usually a sign you're using it for the wrong things — or that you need more permanent capital, not more revolving access.

4. Ask what the money will actually do before you draw. Is this replacing revenue you haven't collected yet? Line of credit. Is this buying something that will generate revenue over time? Term loan. Is it covering a one-time gap while a large contract funds? Line of credit. Is it funding growth with a concrete return and timeline? Term loan. If you can't answer that question clearly before you sign, slow down.

5. Think about what your debt looks like to a lender or buyer 18 months from now. Before you take on any new facility, run this test: if a bank underwriter or a prospective buyer looked at this debt today, would it make sense? Would the structure tell the story of a business that borrows with intention? If not, that's worth pausing on before you commit.

Most funding mistakes aren't about taking too much capital or too little. They're about using the wrong tool for the job — and not realizing it until the next conversation with a lender is harder than it should be. If you're looking at a capital need right now and want a second opinion on which structure fits, or if you've got existing debt you want to sanity-check before your next application, I'm happy to take a look. Explore your options → baysidebusinessadvisors.com/explore-options