What Your Personal Credit Score Is Really Costing Your Business — And How to Fix It Before You Apply

Most business owners assume their business is the loan application. It's not. You are.

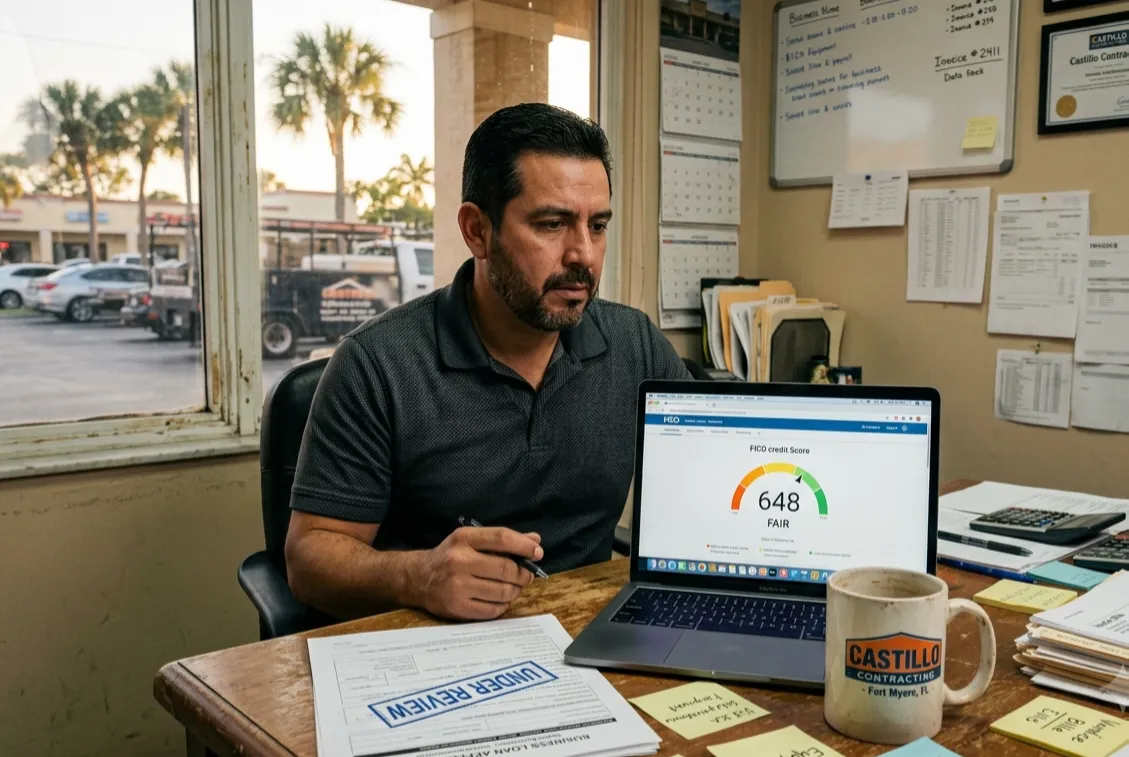

When a lender pulls your file — bank, SBA, or non-bank — the first thing they look at isn't your revenue. It's you. Your personal FICO score, your payment history, how you've handled debt when things got tight. That single number either opens the door to your cheapest capital options or slams it shut before you've said a word. If you're running a $500k–$5M service business in South Florida and you haven't looked at your personal credit in the last 90 days, you're flying blind into one of the most consequential decisions you'll make for your business.

Here's what's actually happening — and what to do about it before you need the money.

What Lenders Actually See When They Pull Your File

Credit isn't one number. When a lender reviews your loan application, they're looking at a layered picture: your personal FICO score, your business credit profile (through Dun & Bradstreet, Experian Business, or Equifax Business), and in some cases a combined score called the FICO SBSS — a 0–300 metric that blends your personal credit, business credit, and financial data into a single risk signal.

As of March 1, 2026, the SBA officially sunset the mandatory SBSS score requirement for 7(a) Small Loans under $350,000. But here's the thing: most SBA lenders are still using it voluntarily because it's baked into their underwriting systems. And for larger 7(a) loans, the full review process — including personal credit — is more rigorous than ever.

Here's the practical reality of where scores land in 2026:

Below 620: SBA doors are largely closed. You're looking at alternative lenders with APRs that can hit 40–80%, or MCA territory.

620–649: You may qualify for SBA Express or Microloan programs, but options are thin and rates are near ceiling.

650–679: You're in consideration for most 7(a) programs. Lenders will want compensating factors — strong DSCR, collateral, time in business.

680+: You're a real candidate for SBA 7(a) and SBA 504 on favorable terms. Lenders have real flexibility to work with you.

700+: You're competitive. Lenders will move faster, rates will be lower, and you may avoid collateral requirements on smaller deals.

One of my clients — an HVAC contractor in Broward County doing just over $900k a year — came to me wanting a $350,000 SBA 7(a) to buy out a retiring competitor. Business was profitable, the deal made sense, and he had a real down payment ready. But his personal FICO was sitting at 638, and he had three late payments from two years back when a large account went slow on him. We had to work around the SBA route entirely, which cost him roughly two percentage points on his rate and added a personal collateral requirement that wouldn't have been triggered above 680.

That gap — 638 to 680 — cost him tens of thousands of dollars over the life of the deal. And he had no idea his personal credit was the problem until he was already in the process.

Why Owners Get This Wrong — And What It Costs Them

The most common mistake I see: owners treat their personal credit like a personal finance issue, not a business tool. They're focused on revenue, payroll, and operations — and the credit report sits untouched until the day they need capital. By then, it's too late to fix anything.

Here's what most owners don't realize:

Your personal credit affects every category of business financing. SBA loans require a personal guarantee from all owners with 20%+ stake — and that personal guarantee comes with a personal credit review. Non-bank lenders use your FICO as a primary risk signal. Even traditional term lenders who claim to underwrite on "business fundamentals" almost always run your personal credit early in the process.

Thin business credit makes the problem worse. Newer businesses — under three years — often haven't built up a business credit profile at D&B, Experian Business, or Equifax Business. When lenders don't see a business credit history, they weight your personal FICO even more heavily. So if your business is 18 months old and your personal credit is at 650, you're carrying double exposure.

It damages SBA eligibility at the worst time. There's a pattern I've seen repeatedly: owner has a profitable business, gets a cash advance during a slow stretch, makes payments consistently, but meanwhile personal credit slides because they stopped paying attention to utilization or let a personal card balance creep up. Twelve months later, they're SBA-eligible on every metric except the one that quietly disqualified them. By the time they apply, the damage is already done — and it takes 12–24 months to fully recover a score from significant derogatory marks.

It affects your exit. If you're planning to sell your business in the next 2–5 years, here's something your broker may not tell you: many buyers of small service businesses finance the acquisition through SBA loans. If your business history includes poor credit decisions at the ownership level — unpaid judgments, tax liens, derogatory personal marks — sophisticated buyers will flag it as risk and may walk from the deal or recut the price.

What to Do Before You Apply

You don't need to be a credit expert. You need to spend two hours on this before you ever submit a loan application. Here's exactly what to do:

1. Pull all three personal reports. Use AnnualCreditReport.com — it's the only federally authorized free source. Look specifically for: late payments in the last 24 months, any collection accounts, judgments or tax liens, and your credit utilization rate (balance divided by limit) across all accounts.

2. Check your business credit profile. Pull your D&B file at DNB.com and your Experian Business report. If you don't have a profile, that itself is information — it means lenders will rely more heavily on your personal credit.

3. Target 680 before you apply. If your score is below 680, you have specific levers: pay down utilization below 30% on personal cards (this alone can move a score 20–40 points in 60 days), dispute any errors in writing, and avoid opening new credit lines in the 90 days before you apply. Do not close old accounts — they hold your credit age and hurt you if removed.

4. Resolve any tax liens or judgments now. A federal or state tax lien is a hard stop on SBA eligibility. If you have one, it needs to be paid or set up on a formal repayment plan before you apply — not the week of.

5. Talk to an advisor before you apply. An experienced capital advisor will pull your credit picture with a soft pull, walk you through exactly where you stand, and tell you whether to apply now or wait 60–90 days. That conversation takes 30 minutes and could save you two points on your rate and tens of thousands over the life of a loan.

The Bottom Line

Your personal credit score is not a personal finance metric. It's a business tool — and for South Florida service business owners trying to access SBA loans, non-bank term debt, or credit lines, it is one of the highest-leverage things you can manage between now and your next capital raise.

The owners who show up to a funding conversation with clean credit — 680+, current on everything, business profile established — get better rates, more options, and faster closes. The ones who haven't looked at their report in two years often find out about problems only when a lender declines them or reprices a deal upward.

Check your numbers. Fix what you can. Then come to the table ready.

If you want a second set of eyes on your credit picture before you apply — or you're not sure whether your current score puts you in range for the capital you need — we are glad to walk through it with you. No pressure, no commitment.